September 30, 2002

|

|

||

|

|

|

|

|

|

||

|

Home >

Money > Special September 30, 2002 |

Feedback

|

|

|

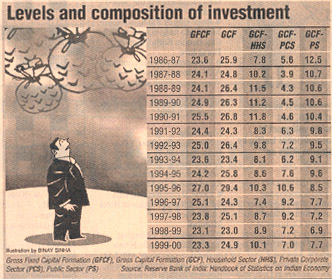

The investment droughtSubir Gokarn The monsoon has come and gone. It raised the spectre of drought by its early performance, but set some of those fears at rest by its subsequent recovery. Even then, the earliest indications of crop performance are fairly negative, but a complete and reliable picture is not yet available. All one can say at this stage is that the early fears were probably unfounded. The good news is that rainfall inadequacy is not a persistent structural problem. Unfortunately, one cannot say the same thing about the economy's performance on an indicator, which is critical to both short-term and long-term performance: investment. There has been much ado about foreign direct investment in the last few weeks. The report of the steering committee on FDI, chaired by N K Singh, was submitted to the government. Its specific recommendations for increasing FDI inflows included raising the investment limits across a range of sectors, many going up to 100 per cent, and allowing foreign investors to participate in the divestment process. The acceptability of such recommendations was put to an early test, when the Cabinet considered raising the FDI limits in aviation, telecom and insurance. They did not pass. Meanwhile, international comparisons demonstrated India's relative unattractiveness as a potential investment destination. The World Investment Report, published annually by UNCTAD, ranked India 104 on FDI potential and 119 on FDI performance (out of 140) for the period 1998-2000. Interestingly, for 1988-90, India was ranked 96 on potential and 121 on performance. The large movement of the ranking on potential reflects the fact that, even as India has been going about its reforms, other countries have made their domestic environments more hospitable for FDI. Meanwhile, the FDI Confidence Index, put out twice a year by the consultancy firm A T Kearney, showed India dropping to 15th place after having been in the top 10 (with a high of 5) over the last couple of years. This index is based on the perceptions of the managers of large multinational corporations, which account for a significant proportion of global FDI flows. There is likely to be strong correlation between the ranking on this index and the magnitude of inflows over the next two or three years. Ironically, there appears to be something of an upsurge in inflows into India recently, but closer examination suggests that this is largely by way of existing investors consolidating their holdings. Not much is coming in for purposes of new capacity creation. So, now we should all be persuaded that India is not a very hot destination for FDI. But let's change focus for a moment and look at investment in totality. Is India a hot destination for domestic investment? If it is, then, clearly the FDI policy priority should be to reduce the barriers that are specific to foreign investment. But, if it isn't, then the more relevant question is: what makes India unattractive for investment, foreign or domestic? Surely, with reference to a given business environment, you can't really expect foreign investment to flow if domestic investment itself is reluctant? The table provides some indication of the performance of investment over the last decade and a half. There are four variables displayed, all expressed as a percentage of GDP.

The first column shows Gross Fixed Capital Formation, which is a measure of the resources being devoted by the economy to create capacity for future growth. The second shows Gross Capital Formation, which is the sum of GFCF and inventory accumulation. The reason for putting this into the table is that the decomposition displayed in the next three columns is available for GCF but not GFCF. The next three columns show the relative significance of three sectors in investment activity: households, the private corporate sector and the public sector. The data on capital formation is not yet available beyond 1999-2000, but the story is unlikely to change. Based on the patterns in the table, a number of points can be made. Firstly, from the first two columns, it is clear that the Indian economy has never had anything resembling an investment boom. Except for a year or two, total investment in the mid-to-late 1990s more or less reached the levels of a decade ago, after the dip in the early 1990s. However, the composition of the investment was quite different in the later period. Public investment over the 1990s shows a steadily declining pattern. This started out as a well-intentioned programme to de-emphasise the public sector in favour of the private sector in infrastructure, but, in hindsight, is significantly responsible for the overall deterioration in that sector. Public investment is widely believed to "crowd in" or facilitate private investment by making the climate more attractive. If this is true, we don't have to look very far for an explanation for the increasing unhealthiness of the climate. Private corporate boomed in response to the reforms of 1991. Even now, it is somewhat higher in proportionate terms than its levels of the late 1980s. But, there is a clear downturn in the late 1990s. Since this is predominantly domestic, it indicates an increasing sense of scepticism amongst investors at home about the viability of their projects. Why, then, would we expect foreign investors to feel any differently? The private investment boom was driven by the promise and prospect of continuing reforms, which would deal with the many sources of high cost and uncertainty prevalent in the Indian business environment. As that prospect petered out, so did actual investment flows. Household sector investment captures two distinct activities. The first is expenditure on housing itself. This fuels demand for construction services, with all its linkages to industry, and is therefore an important source of short-term demand stimulus. However, it does not directly enhance the productive capacity of the system and therefore does not offer the prospects of faster growth in the future, which investment in machinery, equipment and infrastructure do. The second is investment in productive assets in the informal manufacturing and services sector. This does generate employment, so again, it has a short-term payoff. However, relative to the private corporate sector, its long-term prospects are limited because of constraints on its abilities to assimilate new technology and persistently increase the productivity of its workers. The bottom line is that both the level and sectoral pattern of investment in India are not conducive to accelerating the growth rate and sustaining it at that level. But, there are welcome signs of an impending cloudburst. The Tenth Five Year Plan offers some redressal of the balance with respect to investment in roads and power. The report on FDI offers a set of recommendations on policy, procedure and regulation, which will do just fine for domestic investment, leave alone FDI. Labour market reforms remain uncertain, but the debate is moving into the realm of pragmatism. Like the monsoon in August and September, will policymaking also do some rainmaking? ALSO READ:

|

ADVERTISEMENT |

||||||||||||