While buying a term plan, do check how much money will be paid in lumpsum and how much of the money will come to the surviving family as a regular payout, suggests Sarbajeet K Sen.

Buying term insurance is essential if you have dependents.

However, the complication arises when you have to choose from multiple claim settlement options.

And since you have to choose this at the time of buying the policy, things get trickier.

What is on offer?

A term insurance policy in its purest form pays the nominee a fixed sum assured if the life assured dies during the term of the policy.

The premium paid is forfeited in case the life assured survives the policy term.

It covers the risk of dying early at the lowest possible premium.

It gets a bit twisted when the buyer is asked how the life insurance company should settle the claim.

Life insurers offer three popular means of settling the claim.

You may ask the life insurance company to make a single payment and pay the entire sum assured in one go.

Or you can also ask the life insurance company to pay a combination of a fixed sum and installments thereafter.

Under this, there are two options available.

The nominee is paid a fixed sum and an assured monthly fixed payout for a stipulated period of time (say, 10 years) or the life insurance company may pay a fixed sum and an increasing monthly payout (say, rising at 3 per cent a year) for a stipulated period of time (say, 10 years).

"The staggered payout is preferred when the policyholder feels that his dependents will not be able to manage their finances well upon receiving the lumpsum amount at a go," says Santosh Agarwal, associate director and cluster head - life insurance, Policybazaar.com.

"The staggered option also helps them take their financial decisions in a planned way through different variants including monthly income, increasing monthly income, lumpsum with monthly income and lumpsum with increasing monthly income," Agarwal adds.

Impact on premium outgo

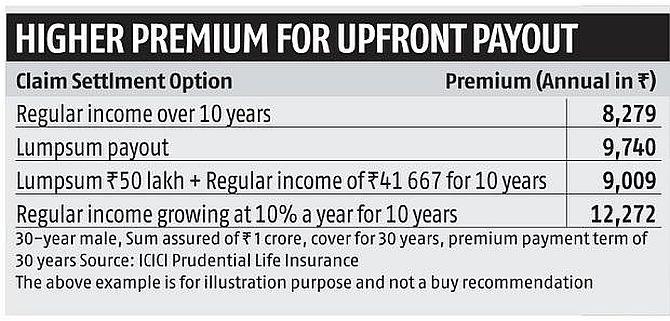

"In the case of term insurance, the mode of receiving claim amount can affect the premium.

"If you go for the lumpsum method then you have to pay a slightly higher premium for it," says Naval Goel, chief executive officer, PolicyX.com.

In short, earlier you expect the insurer to pay the benefit upon the death of the life assured, higher the premium.

For example, other things remaining the same, the premium payable on lumpsum payment of sum assured upon death will be higher than the premium payable on a combination of lumpsum and regular income thereafter (Please see table below).

Why are these options on offer?

Insurers have realised that paying the entire sum assured at one go does not help the nominee.

Only a few individuals understand how to handle large sums of money.

Many times such large sums disappear as the family could not set the priorities right due to lack of financial literacy.

To overcome this, the buyer may choose to stagger payout to the survivors.

In that case, he may choose the claim settlement option of lumpsum and regular payment.

"Lumpsum option is most often selected by the policyholder. However, many family members do not have the required knowledge when it comes to handling a large sum of finances, and they are most unlikely to make the best use of the lumpsum," says Vineet Arora, MD and CEO, Aegon Life Insurance.

"To overcome this concern, the policyholder can opt for monthly or periodic payout option where the beneficiary receives some portion as lumpsum and the remaining amount can be received regularly as income," adds Arora.

In most cases, individuals do borrow to fulfill their financial goals.

Be it the purchase of a house, getting a family member married or even for the education of a family member one may have raised some loans.

In case of unfortunate death of the primary earner, before s/he repays the debt, the family members may find it difficult to repay without pulling down their lifestyle.

The lumpsum component received as claim settlement can be used to take care of large expenses, including repayment of large outstanding loans.

Other large expenses include relocation expenses, purchase or renting alternate accommodation in case the existing accommodation is employer provided and settling impending liabilities.

The regular income can be utilised by the family for its day to day expenses.

Which one should you choose?

If you have large debt pending in your name, it is better to arrange for the repayment of the same in case you are not around to provide for it.

In that case, the lumpsum claim settlement option looks good.

However, if you are not sure about how your family will utilise the large sum in your absence, then it is better to go for the combination of lump sum and regular income payout option.

"The thumb rule that can be advised is that where large liabilities are required to be paid off, it is advisable to go with the lumpsum payout. However, if one wishes to ensure regular income for the family the staggered payout plan fits the bill," says Arora.

While buying a term plan, do check how much money will be paid in lumpsum and how much of the money will come to the surviving family as a regular payout.

Once you choose the option, it is generally binding on you.

Do not select a term plan claim settlement option looking at the premium.

Cheaper means your family will be paid regular sums instead of a large lumpsum, even if they need a large amount to settle some due.

© 2025

© 2025