Have you realised how close you are to July 31? It might not seem very close, but there are barely five weeks to go. By then, your income tax returns should be filed for financial year 2008-09.

So, if you or your chartered accountant have not yet started calling up each other about your tax returns, it's about time you made the first call. It makes no difference whether you are working abroad at the moment: if you have any taxable income in India, it is time to pull up your socks.

Typically, filing tax returns can be boring and complex with the added threat of penalties and harassment if you do not get the maths right. To come out smiling, all you need is a bit of preparation. The government expects you to have paid taxes on whatever you had earned, spent and invested in the last financial year.

And it expects you to have done so on or before the last date for filing returns. All taxpayers need to file back or report any such income or expense details with the government in a prescribed format.

Last year's Budget had much to offer to salaried taxpayers of the country and helped in saving the tax outgo.

There were two ways in which the taxpayer benefited. One, the threshold level of income tax went up. This means that a greater part of the income comes under the zero tax category. To make the tax pill even sweeter, tax slabs were raised very generously as well.

Earlier, the maximum marginal rate of tax of 30 per cent was applicable from the annual income level of Rs 2.5 lakh (Rs 250,000). This now stands doubled at Rs 5 lakh (Rs 500,000) for the financial year 2008-09. This means that instead of incomes over Rs 2.5 lakh being taxed at 30 per cent, now the part of income that is over Rs 5 lakh will be taxed at 30 per cent.

This means a male taxpayer less than 65 years of age, with a gross income of Rs 5 lakh, will now save about Rs 44,000 in income tax.

But then, how do you file the return? First, identify all your sources of income. You may earn a salary and have capital gains as well, if you are dabbling in shares.

Also, if you have taken a home loan, the head 'income from house property' also needs to be accounted for. Therefore, identifying the heads of income is the first step.

Then, keep documentary evidence handy for any income, expense or deduction on which you have taken a tax benefit.

Running around to gather them at the last moment is certainly troublesome and should be avoided as much as possible by making the process simpler and less energy consuming.

Next, place the figures under each of the income heads and get your gross total income. From the gross income, reduce any deduction under Section 80 of Income Tax Act.

The gross income that remains is the taxable income on which the tax needs to be paid. Based on who you are -- a woman, a senior citizen or 'other' -- the tax liability would differ.

Computing this could be slightly tedious, but help is available both offline and online. Following this, depending on the income source, choose the appropriate ITR form that needs to be filled up. Finally, choose to go either offline through your neighbourhood chartered accountant or online through any of the designated websites.

When it comes to the actual filing, you can easily fill up the form yourself and submit it to the income tax office.

If that's sounding tough, there are three roads to choose -- help from a chartered accountant, a tax return preparer (TRP) or through a designated e-filing website. E-filing websites are designed to cut through the maze of difficult tax jargon.

These sites hold the taxpayer's hand while he files the returns on his own. This makes the process faster and educative.

The language of taxation intimidates lay persons, who see it as a complicated subject. In the last 10-15 years, our taxation system has undergone tremendous reforms and the tax structure now is well organised. Each year the base of taxpayers is increasing.

From 3,01,78,000 in 2003-04 to 3,25,00,000 in 2007-08, the number of assessees has increased.

If you are a new taxpayer or one who is struggling to obtain a foothold in the world of taxes, our attempt at simplifying the tax filing process seeks to help you sail through this. Read on. . .

Powered by

Step 1. Identifying your sources of income under these income heads.

Place a tick mark against the relevant item

Powered by

Step 2. Keeping documents ready

Check out which documents you need to keep handy in order to calculate your tax.

Which Documents To Keep?

Identify your income sources and place them under the right income heads. Accordingly, you would need documents. Here's a list.

Income from Salary

Income from House Property

Income from Capital Gains

Income from Business/Profession

Income from Other Sources

Powered by

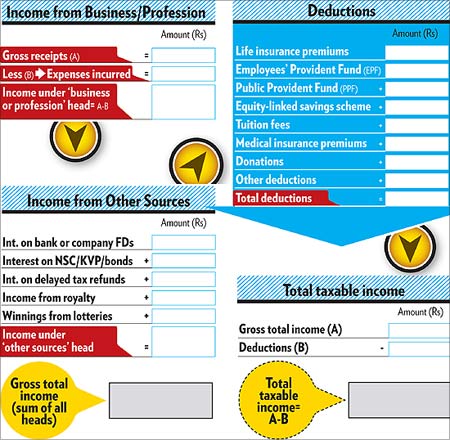

Step 3. Computing the gross total income (GTI)

Add up your earnings from the five income heads to arrive at total taxable income.

How to compute your taxable income

We have prepared a worksheet for you, wherein you can fill in your income and expense details under various heads and compute your gross total income, deductions and total taxable income.

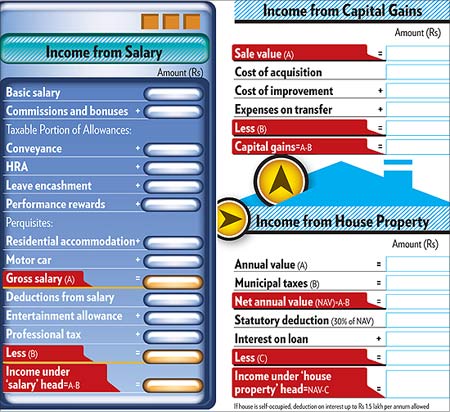

Now that you have got your papers in order, how do you calculate your tax liability and figure out whether you need to pay more tax, get a refund, or have done it right? To do that, you will have to add up your total earnings from various income sources. This will give you the gross total income. To get your total taxable income, you will have to subtract the standard tax deductions (Section 80) from the gross income. Here's a look at the five income heads and what they include.

Income from salary

Gross salary includes basic salary, commissions, allowances and perquisites. Subtract certain deductions from this. The balance is charged under the head 'salary income'. Your basic, allowances, commissions and bonuses are fully taxable.

Powered by

Step 4. Calculating deductions

Add up all your Section 80C and non-80C deductions.

House rent allowance (HRA). This is exempted up to a certain limit if you are actually paying house rent. The lowest of three amounts, actual HRA received, rent paid in excess of 10 per cent of basic salary, and 40 per cent of your basic salary (50 per cent for Mumbai, Kolkata, Delhi and Chennai), would be exempted. Conveyance allowance up to Rs 800 per month is exempt from tax.

Leave travel allowance (LTA). It is a reimbursement for travel expenses that you and your family members incur within India while you are on leave. While LTA can be paid to you every year, it is treated as tax-free only for two journeys in a block of four years. Both these journeys can be made in any one of the four years or spread out over the four years.

Powered by

Step 5. GTI minus deductions.

Medical allowance. Reimbursement of medical expenditure incurred by you and your family is tax-free up to Rs 15,000 per annum. All reimbursements need to be supported by bills.

Perquisites. These are benefits that you get in addition to your regular salary. These are usually in the form of accommodation, car and concessional loans. The total of all perquisite values is added to the salary and tax is calculated on the usual slabs.

Premium for group medical and term insurance paid by your employer escapes the tax net. However, you need not worry about calculating all this. Your employer will give you Form 12BA, which will show the value of your perks as part of your salary.

Powered by

Step 6. Calculating total taxable income

Income From House Property

Rental income from a residential or commercial property that you own is taxable. If you have more than one house property and one is self-occupied, then even if the other properties are not rented out, they will be treated so and the implied rent, based on annual value of the property, will be taxed.

The gross annual value is the highest of the municipal value, the actual rent, or the fair rental value. Preferential treatment is given to one self-occupied house, whose annual value is taken as 'nil'. The interest payable on home loans is tax-deductible up to Rs 1.5 lakh a year.

Income from capital gains

Now, let's assume you made certain capital gains last year. If you held real estate, gold or silver for more than 36 months, they will be termed as long-term assets. Otherwise, they are short-term assets.

However, shares and equity mutual funds (MFs) are short-term assets if you hold them for a year or less and long-term assets otherwise.

Short-term capital gains are included in your gross total income and taxed according to the slab in which your income falls. Except listed securities, long-term gains made from all other asset categories are taxed at 20 per cent with indexation.

Gains from shares or equity MFs are tax-free in the long term. These gains are taxed at 15 per cent in the short term, provided, of course, that the securities transaction tax has been paid.

Powered by

Step 7. Calculating tax payable

Your total tax liability may stand reduced if some tax has been deducted at source (TDS). Subtract TDS from your total tax liability to get the final amount to be paid as tax.

Income from business/profession

In case you have income from a business or you are in a profession, the excess of gross receipts over expenses incurred to earn it will be taxed under this head. A person earning his living in a profession such as law, medicine, engineering, architecture or technical consultancy, whose total gross receipts from that profession exceed Rs 1.5 lakh per annum, is required to maintain books of accounts.

Income from others sources

Usually, any income that does not fall under the four heads of income mentioned above is taxed under this head. Examples of such income are, interest earned on bank fixed deposits, savings account and National Savings Certificates.

Now that you have the numbers right, you can proceed to the final act of actually filing your taxes.

Powered by

Step 8. Finding your tax rates

Check out how the separate categories of women, senior citizens and 'others' are taxed.

How much tax to pay?

Individual taxpayers are catgorised as women, senior citizens and others. Identify your category and check out your tax liability according to the tax slab applicable for assessment year 2009-10 or financial year 2008-09

Tax rates for ALL except senior citizens and women

Tax rates for Senior Citizens

Tax Rates For Women

Taxable income level

Powered by

Step 9. Choosing the correct income tax return (ITR) form.

Based on your income sources, you need to choose your ITR form.

The Final Act

Once the documents and the maths are done, the process of filing tax enters the final phase. Get going now instead of getting bogged down later.

Which form to fill?

The return form that you would need to fill will depend on your income sources:

How to file your returns?

You can file your returns offl ine or online. However, before doing so, check whether you still have a tax liability. In you are still to pay taxes, do so through Internet banking or through cash/cheque at any bank along with Form 280.

In both cases, you will get a receipt number which will have to be quoted in your income tax return (ITR) form

Offline

If you want to send tax details to the IT department online and don't have digital signature (DS):

Now that you have sorted out the documents needed to file your tax returns and worked out the mathematics, you just have to transfer the necessary information to the income tax department in the prescribed format by filling out a tax return form and depositing it.

Once that is done, your task is over -- for this year. Here's what to do:

Which form should you use?

There are two income tax return forms, ITR-1 and ITR-2, for salaried individuals. Your sources of income (they will fall under one or more of the five income sources mentioned in the earlier articles) will decide which form you need to use.

Use ITR-1 to file your tax return if your income is from salary, pension or interest. In case of any capital gains, income or loss from house property and income from any other source, you will have to file ITR-2. You can go to www.incometaxindia.gov.in/download_all.asp to download any of these forms.

You will find ITR-1 fairly simple to fill. A prerequisite for the exercise is Form 16, the certificate that comes from the employer. It shows the tax deducted at source (TDS) from the income chargeable under the head salary.

ITR-1 is almost a replica of Form 16. You just have to pick the numbers from Form 16 and put in the ITR form.

That's the end of your job. After this, all you have to do is deposit this form. You will need to fill up ITR-2 if you, as a salaried individual, have made any capital gains. That would require putting in the Form 16 figures in ITR-2 in the same way as you did in case of ITR-1.

In addition, you will have to fill in the capital gains or income, if any, from house property and securities.

If your income is from business or profession, which means that you are not a salaried person, you will need to use ITR-4. This form is slightly more complicated than the other two and you will possibly need the help of someone trained in preparing a tax return, preferably a chartered accountant (CA).

Powered by

Step 10. Filing returns

You can file your returns offline or online.

Remaining Tax Liability

Subtract your TDS from the tax liability that you computed earlier to ascertain if you are still to pay any taxes. If you still have a tax liability, get hold of Form 280, fill it up and deposit it in any bank along with the tax payable in cash or cheque before filing your returns.

You can also pay this through Internet banking. In both cases, you will get a receipt number, which has to be quoted in the ITR form.

What to do for refunds?

If you are entitled to a tax refund, in addition to your contact details, enter your bank details in the form. It is equally important to mention the MICR number of your bank branch. MICR is a 9-digit number mentioned next to the cheque number in the cheque leaflet. If you file your return on time, you will get interest on the refund amount from the beginning of the assessment year.

How to file?

The actual filing of return can be done either by using the traditional paper form or electronically over the Internet.

Offline: Under the offline method, you will have two options -- you may either submit the ITR form at the nearest income tax office (ITO) after filling it up yourself, or you may get a CA or a tax return preparer (TRP) to do it for you.

You may also take help from the public relations officer of the ITO to fill the form. No documents or investment proofs need to be attached with the form, but remember to bring photocopies or originals with you to the ITO.

These will come in handy if you are asked to authenticate your numbers. The CA would charge a fee in accordance with your income slab and the number of income sources. Typically, it would range from Rs 300 to Rs 2,000.

Online: Known as efiling, this method is fast catching up. Ankur Sharma, managing director, TaxSpanner.com, an efiling site, says there has been an increase in efiling this year over last year. "Unlike last year, when efiling picked up only in June, activity has been building up since May this year," he says.

Last year, nearly 4.8 million returns were e-filed. Out of this, 4 million were by individuals and non-corporate entities.

Sharma says availability of digitally signed Form 16 from the employers is making efiling popular. He says: "Employees who have digitally signed Form 16 would simply have to send it to us and their returns would automatically be filed. They wouldn't even need to fill up the form."

Filing returns online is compulsory for companies, but optional for salaried individuals. In the future it will become compulsory for individuals with a certain level of income, so it may not be a bad idea to familiarise yourself with the process.

E-filing process

In order to efile your returns, you will have to input the details of Form 16 in the software of the website, which would automatically generate an electronic return in XML format.

This format helps in sharing of structured data across different information systems. A PDF file of the relevant ITR form is also created along with the XML format on the desktop of your computer. You can download this ITR form, submit it at the ITO and get an acknowledgement.

Alternatively, save the XML file on your desktop and then upload it on www.incometaxindiaefiling.gov.in, the government site. Private sites upload it on the government site on your behalf. You will get the acknowledgement by email.

Using Digital Signature

Using a DS will help you complete the efiling process without paperwork and visits to the ITO. In case DS is used, the acknowledgement is emailed to the taxpayer.

Why DS? Though not mandatory, it is advisable to use a DS for filing your return electronically. A DS authenticates electronic documents in the same way as a handwritten signature authenticates printed documents.

However, using a DS makes efiling a little expensive -- every website has its own charges and it has a validity of one or two years. The cost of DS may be built into the package you choose.

How to get a DS? A DS can be acquired from any of the agencies authorised by the government for the job, including the private and government websites meant for filing tax returns. To get your DS from a tax site, download the relevant form, fill it up, attach the required documents, such as your identity and address proofs, and courier them to the address concerned. The entire process of acquiring a DS may take around 15 days.

E-filing without DS

E-filing without DS is equally convenient now. After filing the returns online, the taxpayer receives an acknowledgment called the ITR-V. Till last year, ITR-V had to be submitted at the nearest ITO, making efiling a manual affair at the end.

From this year, this form just needs to be couriered to a specific IT office in Bangalore making the process convenient for assessees.

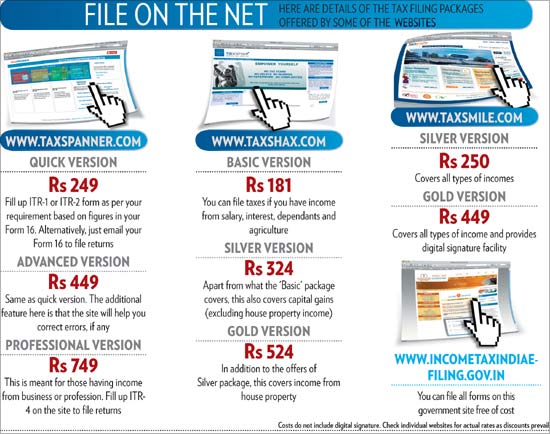

E-filing sites

Among the major sites designated to offer efiling facilities are www.taxspanner.com, www.taxsmile.com and www.taxshax.com. Costs vary across sites.

The government too has a site that offers this facility free of cost. The site is: www.incometaxindiaefiling.gov.in/portal/index.jsp. You will have to use your Permanent Account Number (PAN) as the username for registering on this site.

All the three non-government sites mentioned above are secure and easy to navigate. They are different from each other on two major counts -- the number of income sources they cover and the process.

Get clarity on the cost and features offered before opting for one. Says Ravi Jagannathan, managing director of www.taxsmile.com, "Check if special cases like arrears or clubbing of income are also taken care of." This will save the pain of starting the process all over again.

The cheapest package would normally cover only salary income. You may require the advanced version if you have income from other sources. Taxspanner is the only private site through which you can fill ITR-4, meant for individuals with business or professional income.

Powered by

What to watch out for

Ensure that you have mentioned your PAN correctly. PAN is a compulsory entry in the tax return form. If you have lost the card and forgotten the number too, get your PAN and also a new copy of your card by giving the required information to the income tax department. If you don't have a PAN, apply for it immediately so that you don't miss the tax filing deadline.

If you happened to change jobs last year, remember to report the income(s) from the previous job(s) or Form 16 details of the previous employer(s) as well. Including interest earned on your savings bank account is essential too.

Also, disclosing any share transaction, however small it may be, is a must.

What if you miss the deadline?

In case you miss the deadline of 31 July, you would be left with two options. If there is no pending tax to be paid, you may file your return without paying any penalty by 31 March 2010.

However, if you still have to pay tax and you miss the deadline, you will have to pay a monthly penal interest if you file your return by 31 March 2010. If you cross that deadline too, you will have to pay a penalty of Rs 5,000 along with the monthly penal interest.

Implications: In case you are entitled to a refund, interest on it will be given to you only from the date of filing the return. If you file your returns on time, you can revise your return form to correct any mistakes or deletions, such as missing a particular deduction, by 31 March 2010. However, if you do not file your return on time, you will not be able to avail this facility.

Also, if you have incurred losses on shares during the year, you will be able to carry forward the losses for future tax set-off only if you file the return on time.

Now that you have the necessary details, start the return filing process now, when time is on your side. And relax till the same time next year.

Powered by

Turn of returns

Quick answers to your frequently asked questions regarding filing income tax return.

With the onset of the annual ritual of tax filing, it is time to refresh the checklist for individuals and Hindu Undivided Families (HUFs).

Who has to file tax returns and when?

An individual whose taxable income exceeds the tax-free limit in the financial year ended 31 March 2009 before any claim for deduction must file his tax returns by 31 July 2009. If the individual is subject to an audit, the due date is 30 September 2009.

Where should a manual tax return be submitted? Who should sign it?

The manual filing of the tax return will continue to be in the respective wards of the jurisdictional income-tax office determined on the basis of the place of residence or business.

An individual must sign the return. In case of a minor or a person mentally incapable of doing so, the guardian has to sign. If you are physically absent, you can assign a Power of Attorney to another person to sign on your behalf. For an HUF, the Karta has to sign. If the Karta is absent or is mentally incapacitated from attending to his affairs, any other adult member of the family has to sign.

How is an electronic tax return submitted?

An e-return has to be furnished at https://incometaxindiaefiling.gov.in with or without a digital signature. If you have a digital signature and file directly or through an e-return intermediary, you will not have to furnish form ITR-V with the Tax Department.

If you do not use a digital signature, you need to mail this form within 30 days of the electronic submission to the address: Income Tax Department CPC, Post Box No. 1, Electronic City Post Office, Bangalore-560100, Karnataka. If this is not done, the tax return will be treated as invalid.

What documents are needed with the return?

The Central Board of Direct Taxes has issued a circular recently that taxpayers should not enclose any document with the return. However, you will have to show the documents to the assessing officer if the need arises.

Is it necessary to compile a personal balance sheet and/or a summary of bank transactions?

If a person doesn't have any business income, he need not prepare a personal balance sheet. It, however, helps to keep track of one's assets and liabilities. Similarly, preparing a summary of bank transactions helps in ensuring correct filling of tax return.

How to get credit for advance tax and TDS?

Make sure that all information regarding pre-paid taxes is complete and correct. As per a circular issued on 21 May 2009, a system of Unique Trans-action Number (UTN) and Challan Identification Number (CIN) has been created. It is likely that the UTN information is not included in the TDS certificates since this is a new requirement. Therefore, the taxpayer must get this information from the deductor and ensure that the UTN particulars for each TDS are correctly reported in the tax return.

Is it possible to rectify the mistakes in an already filed return?

You can file a revised tax return by 31 March 2011 or before the assessment is made, whichever is earlier. However, if the tax return is filed later than 31 July or 30 September, no revision is allowed.

What happens if a return is filed late?

If you miss the deadline, you can file a belated tax return by 31 March 2011. But, if there is balance tax payable, you will have to pay interest on the balance at the rate of 1 per cent per month. This can go up to 2 per cent if you have not paid the required advance tax. If you are entitled to a refund, you don't have to pay any interest if you file late.

Any losses claimed (which you cannot set off against your income for that year) will lapse. You will not be allowed to carry them forward to subsequent years.

What is the penalty for delaying or not filing a tax return?

A penalty of Rs 5,000 will be levied if the return is not filed by 31 March 2010. But, if there is a reasonable cause for delay, the penalty may be waived. You can also be prosecuted if the tax payable (net of advance tax and TDS) is above Rs 3,000. You can also be imprisoned for three months to three years, besides being fine. So, it pays to start preparing tax returns early.

The author is a Mumbai-based member of Bombay Chartered Accountants' Society (BCAS), a voluntary organisation of chartered accountants engaged in educating professionals and the society at large.

Powered by

But wait before you file returns! Do you have the UTN?

Assessees whose tax is deducted at source will have to wait for some time this year before filing returns as they will be required to quote a new number in the form.

The new number, Unique Transaction Number (UTN), has been made mandatory because there are some lacunae like individuals having more than one permanent account number (PAN), sources said.

The income-tax department has asked individual assessees whose tax is deducted or collected at source to quote the UTN. The UTN will be given by depository NSDL to those whose tax is deducted or collected at source and individual assessees could get the numbers from deductors.

"Assesses must ensure that the deductor and the collector have provided them with separate UTNs in respect of each TDS and TCS transaction," said a recent circular issued by the department.

When asked whether NSDL has started giving UTNs, tax officials said the department has asked the depository to communicate on the progress in this regard by June 30.

Taxpayers still have more than 35 days to file tax returns, so they should wait for their UTN, experts said.

Also, taxpayers will be able to get the claim only if they quote their UTN.

"Therefore, the credit for any TDS or TCS claim will be allowed, among others, if the assessee quotes the relevant UTN for every TDS and TCS claim and the said UTN matches with the UTN in the database of the Income Tax Department, the circular said.

The department has made some changes in the income tax return forms for the assessment year 2009-10, providing a space for UTN.

Welcoming the move, leading law firm Amarchand Mangaldas partner Aseem Chawla said the move is a step towards achieving the larger objective of online tax administration system.

Tax is deducted at source in case of salaried employees, interest earned on fixed deposits in banks and so on.

Powered by