Photographs: Jagadeesh N.V/Reuters

In a research report on Indian IT sector, Ambit Capital says that many big Indian companies such as Infosys and Tech Mahindra underperform on accounting and corporate governance standards.

The report titled ‘The underbelly of Indian IT’, the financial company has categorised such companies in three categories calling them - the ugly, the bad and the not so good based on their corporate governance.

Let’s take a look at eight such well-known companies covered in the report.

…

The ugly side of Indian IT companies

The Ugly

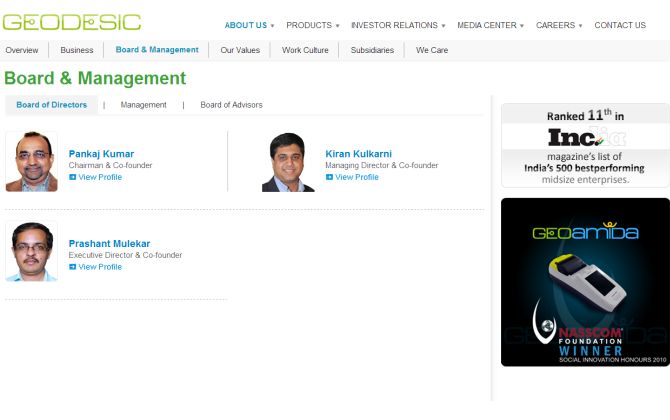

Geodesic: Are the revenues real?

Geodesic’s receivable days have increased to 300 days in FY12 (from 120 days in FY12), whilst the doubtful debt provisioning has increased to 11.9 per cent of debtors (9.8 per cent of revenues in FY12).

Cash yields remain at astonishingly low levels. All these raise concerns whether the earlier year’s revenues were indeed real.

Cash conversion though improved over the last three years, the increase in current liabilities has been a significant factor pushing up the cash conversion.

…

The ugly side of Indian IT companies

Educomp Solutions: Accounts window dressing?

Educomp’s creation of a special purpose vehicle to transfer its receivables and then securitise it was an attempt to improve its cash conversion and make its balance sheet look lighter.

Its change in revenue recognition policy was also intriguing. These coupled with instances of poor disclosures make it an interesting case study.

…

The ugly side of Indian IT companies

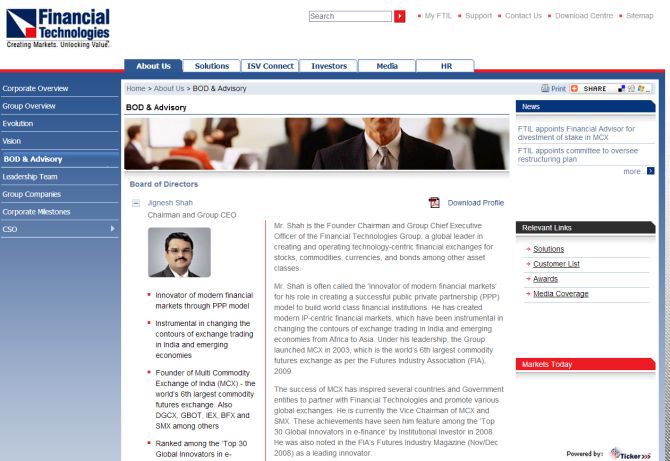

Financial Technologies: Suspicious subsidiary accounts; corporate governance concerns

From a stockmarket darling, riding on success in MCX and similar expectations from the other exchange ventures, Financial Technologies is now struggling to retain ownership of these exchanges on the back of the NSEL fiasco, bringing down expectations from its other exchange ventures.

Besides the corporate governance issues (for not curbing the illegitimate activities at NSEL), our analysis also indicates suspicious manipulation of subsidiary accounts to present a better picture at standalone business.

FT does not publish consolidated quarterly results (despite 40 per cent revenues from subsidiaries), and hence, presenting good-looking standalone numbers makes sense.

…

The ugly side of Indian IT companies

The Bad

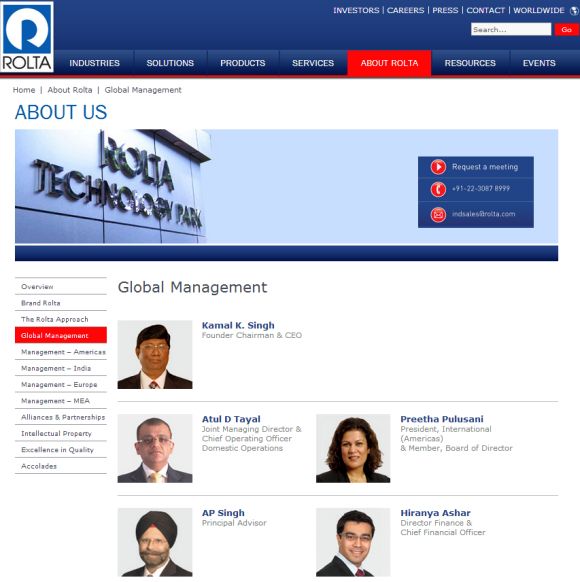

Rolta India: Tricky accounting practices

An analysis of the financial statements of Rolta India indicates a couple of grey areas. Its recent revaluation of land just coinciding with the change in depreciation policy (to bring the depreciation rates to the industry norms) seems to be an accounting trick to manage the net worth, whilst at the same time not hurting the future profitability (as land is not subject to depreciation).

Rolta’s capital employed turnover has also been quite low (0.5x on an average over FY11-13).

A deeper look indicates that despite moderate revenue growth (6 per cent USD revenue CAGR over FY10-13), the capital expenditure has remained surprisingly high (average 46 per cent of revenues over FY11-13). This creates suspicion on expense manipulation (through capitalisation).

Furthermore, Rolta has an uneven accounting history with the SEBI probe on overreporting of revenues through booking of inter-divisional transfer of selfassembled/integrated’ capital equipment as sales.

Though Rolta has abandoned this practice post the SEBI order in 2004, the other observations raise concerns on the sanity of accounting practices.

…

The ugly side of Indian IT companies

Photographs: Vivek Prakash/Reuters

MCX: Suspicious related party deals and seemingly artificial volumes

Whilst MCX has been a success story and the only publicly listed commodity bourse in India with 77 per cent market share, it does not have a clean accounting and operational track record.

The reported volumes seem to be overstated (evident from unnaturally higher Average Daily Volume to Open Interest ratio), whilst transactions with promoter entity do not seem to be at arm’s length.

Lower margin to open interest also reflect imprudent risk control, presumably in pursuit of higher volumes.

Company response: Declined to comment

…

The ugly side of Indian IT companies

Photographs: Danish Siddiqui/Reuters

Tech M: Weaker disclosure norms; accounting not up to international standards; flags on governance

Whilst many see Tech Mahindra as the next tier-1 Indian IT service company, its quality of disclosure lags that of other tier-2 companies such as Mindtree.

TechM does not publish quarterly cash flow and balance sheet statements and it provides no service-line break-up.

Secondly, whilst all the tier-1 firms publish IFRS financial statements, along with the Indian GAAP accounts (with the exception of HCL Tech that reports under US GAAP), Tech Mahindra reports financials only under Indian GAAP.

This makes comparisons with peers less meaningful due to differences in accounting methods.

Finally, lack of adequate independent director representation on the Satyam Board at the time when the swap ratio between Satyam and TechM was finalised raises concerns on corporate governance.

…

The ugly side of Indian IT companies

Photographs: Vivek Prakash/Reuters

Infosys: Letting down its own governance standards?

Ever since its IPO in 1993, Infosys has been regarded as a paradigm of corporate governance in India.

Whilst this image earned Infosys goodwill from investors, clients and employees, there are signs that these high corporate governance standards are fraying.

NRN Murthy’s entry into Infosys in an executive capacity (even after Infosys’ well-articulated policy of executives retiring at the age of 60), bringing with him his son as executive assistant, higher promoter representation at the Board and peculiar guidance pattern resulting in high volatility in the share price - none of this gels with Infosys’ image of a leader when it comes to corporate governance.

…

The ugly side of Indian IT companies

KPIT Technologies: Magnified margins

KPIT Technologies’ margins appear to be overstated given the accounting policies and estimates that are different from its peers.

Its accounting policy of excluding reimbursements both from income and cost (contrary to accounting policy followed by companies such as Infosys, TCS and Persistent Systems) benefits its margins by 50 bps according to our calculations.

Furthermore, its actuarial assumption of salary increase for retirement benefit obligations is significantly below that of peers (5 per cent vs peer average of 7 per cent).

article