The third-quarter financials didn't excite market watchers.

But equity investors can still make money if they invest in the right stocks.

The corporate earnings for the quarter ending December 31, 2022 (Q3FY23) were lower than expected, with a year-on-year (YoY) decline in net profit of non-financial firms (those excluding banks, non-banking finance companies and insurance firms).

This triggered an earnings per share (EPS) downgrade by brokerages after nearly one and half years of earnings upgrade.

EPS refers to how much net profit a company makes for every share owned by its owners and shareholders.

For example, brokerages now expect 26 of the fifty Nifty50 index companies to report lower EPS in FY23 compared to their estimates prior to Q3FY23 results.

In comparison, the rest of the 24 Nifty50 companies are expected to report higher EPS in FY23 compared to previous estimates.

The downgrade/upgrade ratio, is even worse for the Nifty Junior index companies.

This index tracks share price of 50 large-cap companies that are not part of the Nifty50 index.

Brokerages expect nearly 70 per cent, or 34 of the 50, Nifty Junior index companies to now report lower EPS in FY23 than what they had expected at the end of calendar year 2022 (CY22) on December 31.

The biggest downgrade has been for companies in sectors such as metal & mining, oil & gas, life insurance, paint, FMCG, pharma & healthcare, and consumer durables.

In contrast, most of the earnings upgrade has been for banks, auto makers, power and some FMCG companies.

Within the Nifty50 index, the biggest earnings downgrade is seen in Bharat Petroleum Corporation, Tata Steel, and JSW Steel, ranging between 39 and 61 per cent.

For Nifty Junior companies, the biggest downgrade is for Indian Oil Corporation, Indus Towers, and Bandhan Bank.

The downgrade in earnings also led to a cut in the price target for most of the index companies and has been instrumental in a decline in the indices from their 52-week highs reached in December 2022.

Equity investors, however, can still expect to make money if they invest in the right stocks.

Quite a few index and leading non-index stocks are expected to report good earnings in Q4FY23, thanks to their better financial performance in Q3 of FY23.

Thus brokerages have upgraded their EPS for FY23 and have also raised their share price target.

Here is a select list of 10 stocks from Nifty 50 and Nifty Junior indices that have seen the biggest upgrades in their FY23 EPS estimates by brokerages since the end of December 2022, according to the data sourced from Bloomberg.

In fact, all of them have also seen an increase in their FY24 EPS estimates during this period.

In the analysis, companies such as Tata Motors and Interglobe Aviation, which are expected to remain loss-making in FY23 despite an earnings upgrade, have been excluded.

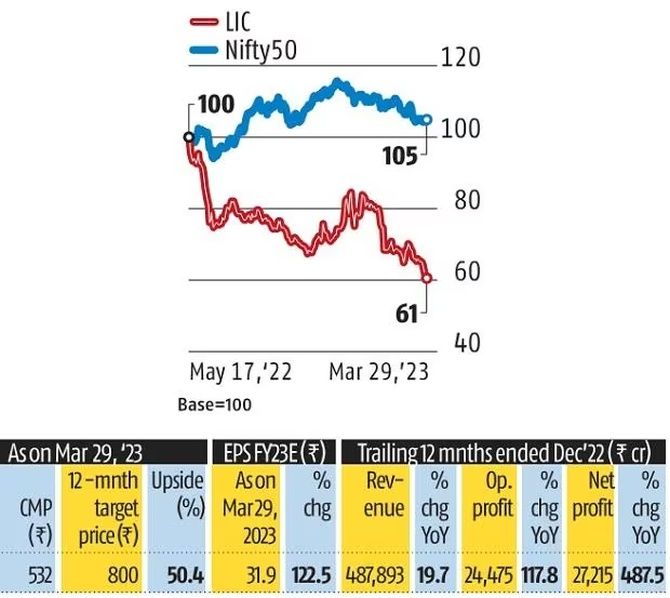

LIC

- Public insurance major Life Insurance Corporation of India has seen one of the biggest earnings upgrades among non-index companies after Q3FY23 earnings.

- Brokerages now expect LIC's FY23 EPS to grow to Rs 31.9, nearly 122.5 per cent higher than its previous estimate of Rs 14.3. They have raised the FY24 EPS estimate by 91.2 per cent to Rs 30.4.

- LIC's earnings growth is expected to be driven by increase in the highly profitable product segments such as protection, non-participating, and savings annuity.

- Brokerages have, however, lowered LIC's target share price to Rs 817.6 from Rs 842.9, in line with the cut in target price of other life insurers.

- LIC's target price is, however, still nearly 52 per cent higher than its current share price of Rs 532.

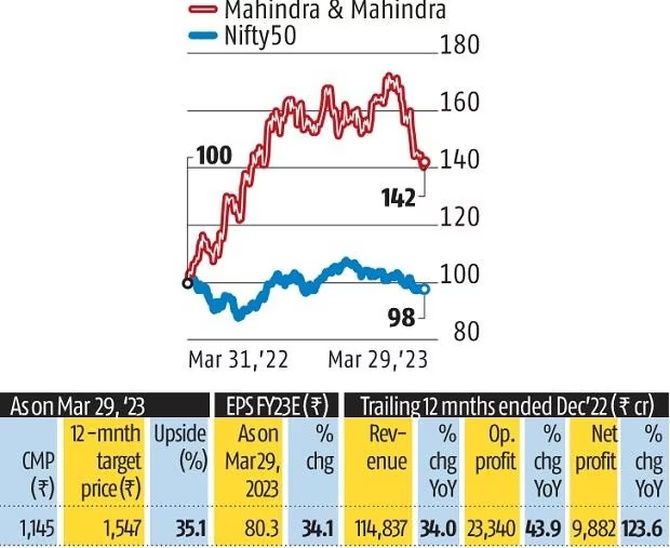

Mahindra & Mahindra

- Higher guidance for tractor volumes, capacity expansion for utility vehicles (UVs), and increase in non-operating income has led brokerages like Systematix Research to sharply upgrade Mahindra & Mahindra's (M&M's) earnings for FY23 and FY24.

- Improved chip supplies, robust demand, and successful launches are positive for the UV segment, which is already seeing higher demand.

- Higher growth guidance this year and market share gains over the past year, led by new launches and network expansion, have improved M&M's position in the tractor segment.

- Lower raw material prices, improving realisation, better product mix and operating leverage are expected to drive M&M's margins going ahead.

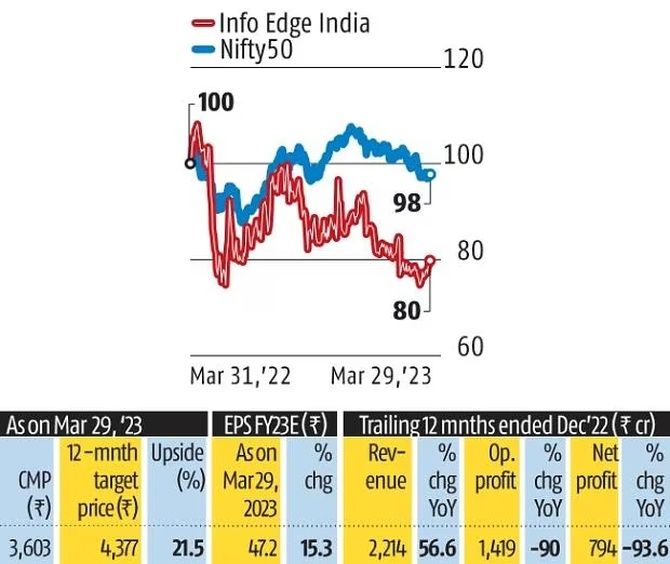

Info Edge (India)

- The recruitment vertical, which accounts for over 80 per cent of Info Edge's revenue, continues to outperform with revenue and margin improvement in the December quarter.

- Even as hiring in core IT (information technology) segment is witnessing a slowdown, the company is experiencing robust demand in non-IT segments such as banking, financial services and insurance, infrastructure, and travel among others.

- The company took an impairment in Q3FY23 related to its investments in 4B Network, which dented the performance for 9MFY23, while the comparable year-ago period had significant gains from listing of investee companies.

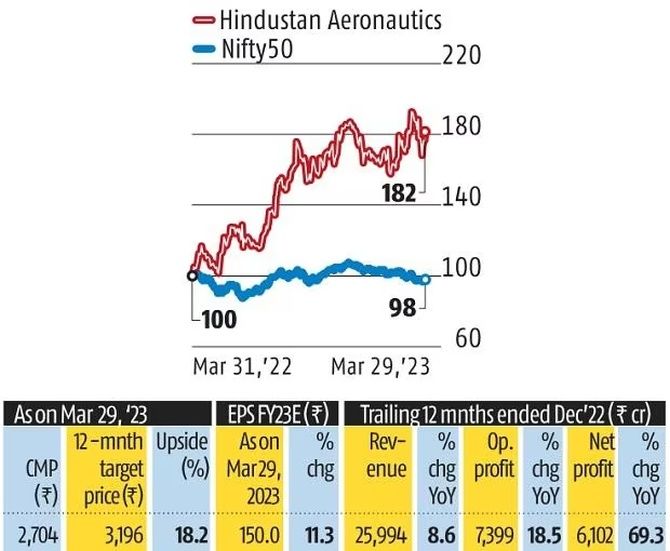

Hindustan Aeronautics

- The upgrades for public sector defence equipment major Hindustan Aeronautics (HAL) are driven by India's focus on indigenisation of defence equipment manufacturing, HAL's emphasis on order execution, and its strong order book.

- Brokerages now expect HAL to report EPS of Rs 150 in FY23, 11.3 per cent higher than the previous estimate of Rs 134.7. For FY24, the EPS is pegged at Rs 153.8 versus Rs 143.5 at the end of CY22.

- HAL's net profit was up 23.1 per cent YoY to Rs 1,153 crore in Q3FY23, while its net sales were down 3.9 per cent YoY.

- Analysts have raised HAL's target share price from Rs 3,141 earlier to Rs 3,196, which is 18 per cent higher than the current share price of Rs 2,704.20.

- HAL, however, is a slow moving giant, and in the last 5 years, its net sales have grown at an annual rate of 6.5 per cent, and the bulk of its earnings growth came from lower raw material costs. Besides, its FY23 EPS is expected to be 2.4 per cent lower than that in FY22.

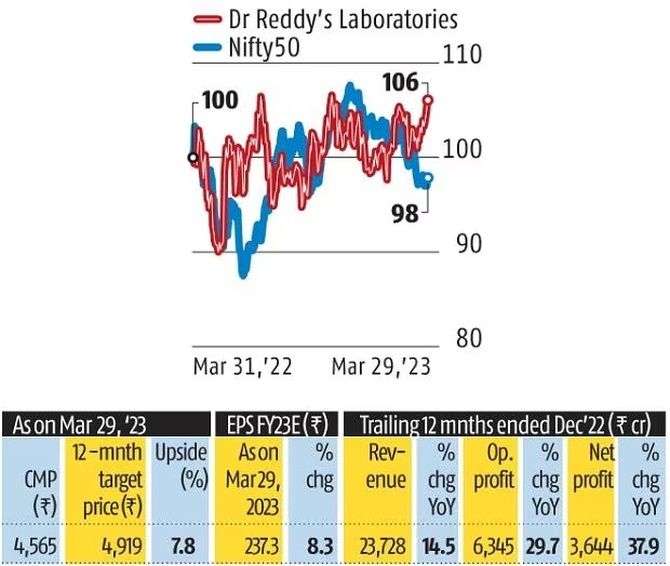

Dr. Reddy's Laboratories

- Riding on higher sales of generic version of cancer drug Revlimid, margins of Dr. Reddy's Laboratories got a boost in the December quarter. Overall US revenue improved as base business also saw a sequential uptick.

- Brokerages expect margins for Revlimid to improve going ahead with lower commodity costs, while new launches should help drive overall revenue in the US market.

- To boost the US base business, the pharma major recently acquired Mayne Pharma's US generic prescription portfolio, which is positive as it offers revenue visibility, and is earnings accretive.

- Ramp-up across geographies on the back of new drug launches, strong free cash flow generation to be driven by Revlimid, and cost approach based on better product mix are key arguments of brokerage ICICI Securities.

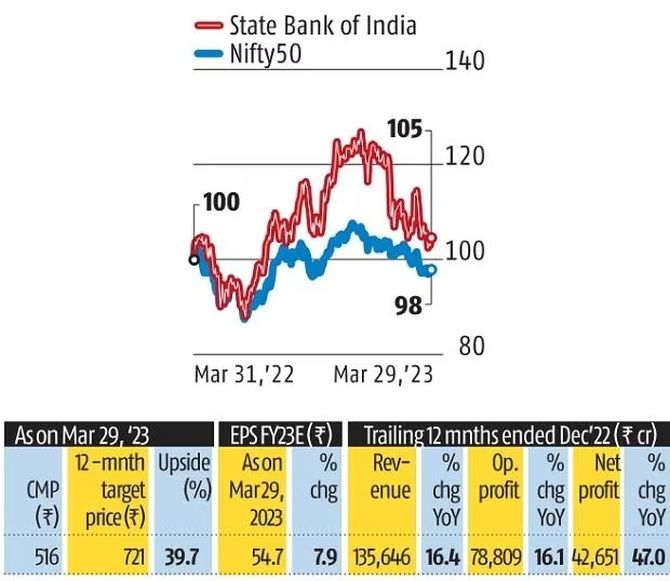

State Bank of India

- After a better-than-expected performance in Q3FY23, analysts have upgraded State Bank of India's (SBI's) earnings estimate for FY23 by 7.7 per cent.

- SBI's net profit was up 68 per cent YoY in Q3FY23, about 7 per cent higher than earlier estimates, while net interest margin was up 18 basis points QoQ (quarter-on-quarter).

- Analysts now expect India's largest lender to close FY23 with EPS of Rs 54.6 as against Rs 50.7 earlier.

- Earnings upgrade is based on the expectation of a further improvement in the banks' net interest income and fee income.

- Brokerages have raised SBI's share price target to Rs 721.4 from Rs 653.4 earlier, which is about 40 per cent higher than its current price of Rs 516.35.

- The expected loss on its bond portfolio from a rise in bond yields has clouded the outlook on SBI's share price.

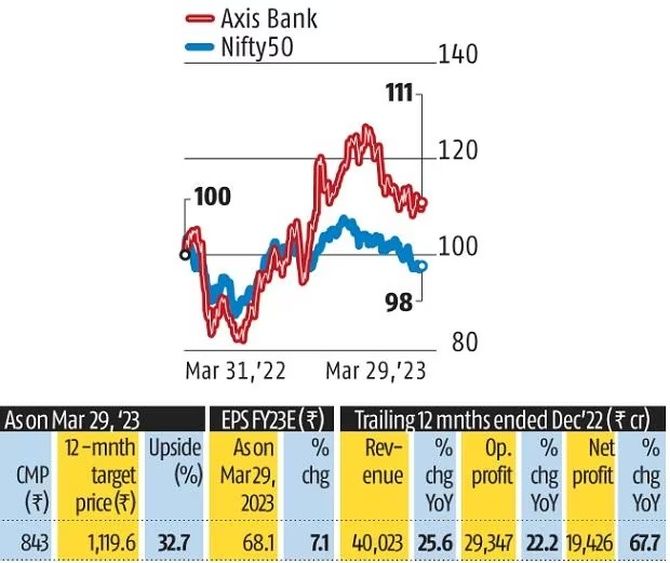

Axis Bank

- Brokerages have raised Axis Bank's EPS estimate for FY23 by 7.1 per cent to Rs 68.1 from the previous estimate of Rs 63.6.

- Axis Bank's net profit was up 62 per cent YoY in Q3FY23, nearly 4 per cent higher than the Street's earlier expectation, driven by faster growth in other income, and margin expansion.

- Brokerages expect the private sector lender to maintain its growth momentum leading to a further improvement in its return on assets and return on equity.

- As a result, brokerages have raised Axis Bank's share price target to Rs 1,119.6 from Rs 1,064.8 earlier. The price target is nearly 33 per cent higher than Axis Bank's current share price of Rs 843.

- The unrealised losses on the bank's held-to-maturity (or HTM) bond portfolio, however, may weigh on its earnings and share price outlook to some extent.

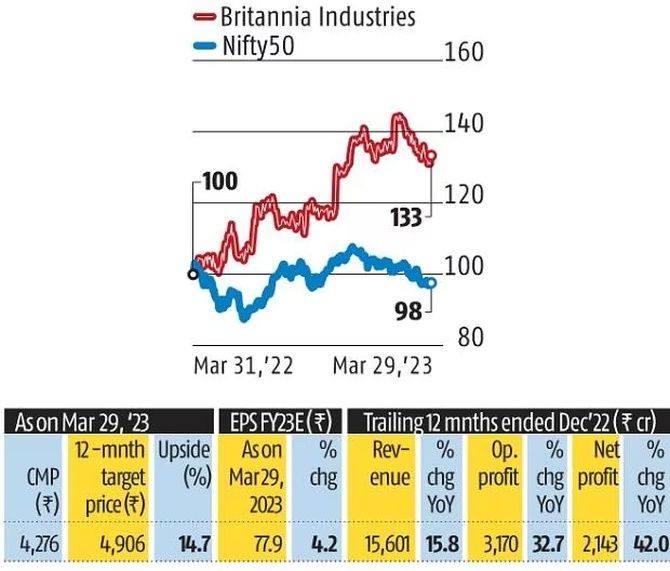

Britannia Industries

- Strong December quarter results, and a healthy outlook on the back of price hikes, and lower raw material costs, led to revision in earnings estimates and upgrades for Britanni.a

- Distribution expansion in the rural segment through addition of rural preferred dealers (28,000 as of December quarter) has helped it wrest market share from competitors.

- In addition to rural expansion and enhanced direct reach, marketing initiatives, new product launches, and development, are expected to help the company sustain its topline performance.

- Medium-term growth outlook, according to Systematix Research, would be led by execution-led share gains in an already outperforming biscuits industry, good traction in new businesses like croissants, milk shakes, and wafers, and aggressive capacity expansion plans.

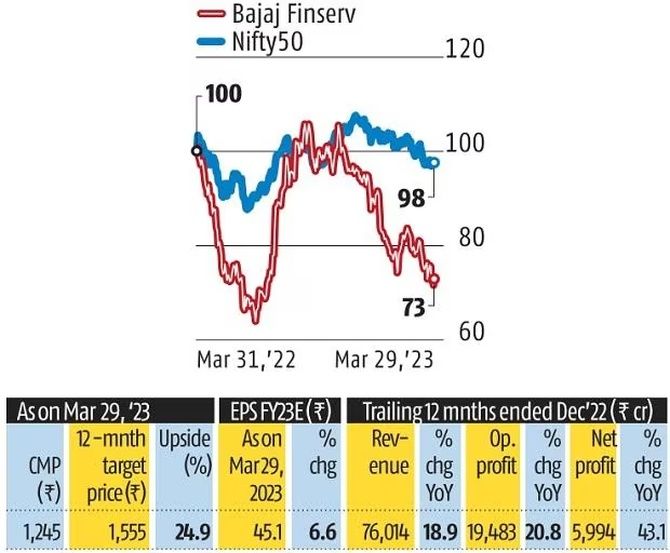

Bajaj Finserv

- Brokerages have raised Bajaj Finserv's estimates of EPS for FY23 by 6.6 per cent after its Q3FY23 results.

- Bajaj Finserv's FY23 EPS is now expected to grow to Rs 45.1 compared to the earlier estimate of Rs 42.3.

- The financial services major's net profit was up 41.9 per cent YoY in Q3FY23, driven by faster growth in its retail financing unit Bajaj Finance, and its insurance business.

- Brokerages have also raised their forward earnings estimate for Bajaj Finance, which accounts for nearly 90 per cent of Bajaj Finserv's consolidated pre-tax profit.

- Many brokerages have, however, cut Bajaj Finserv's target share price to Rs 1,555 from Rs 1,730 earlier, largely due to additional tax on high-value life insurance policies announced in the Budget.

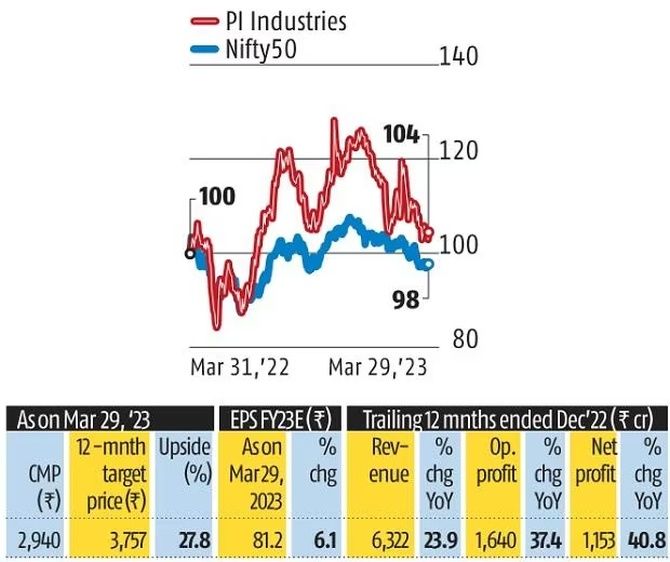

PI Industries

- Led by the custom synthesis and manufacturing segment, better product mix and operating leverage, PI Industries beat the Street's margin expectations for the December quarter.

- Even as the domestic business saw a sequential decline in the quarter, the agrichemicals firm is confident of double-digit growth in FY24 based on launches over the last two-three years.

- A strong balance sheet provides scope for growth over the medium-long term, and its earnings growth outlook remains robust supported by CSM order book of $1.8 billion, ramp-up of nine new products commercialised in the last one year, and launch of new products in FY23, according to Sharekhan Research.

- While valuations are in line with five-year average and thus reasonable, any acquisition in the pharmaceutical space which could drive long term earnings outlook would be an additional trigger for the stock.

Feature Presentation: Rajesh Alva/Rediff.com

Disclaimer: This article is meant for information purposes only. This article and information do not constitute a distribution, an endorsement, an investment advice, an offer to buy or sell or the solicitation of an offer to buy or sell any securities/schemes or any other financial products/investment products mentioned in this article to influence the opinion or behaviour of the investors/recipients.

Any use of the information/any investment and investment related decisions of the investors/recipients are at their sole discretion and risk. Any advice herein is made on a general basis and does not take into account the specific investment objectives of the specific person or group of persons. Opinions expressed herein are subject to change without notice.